ASTANA – Retail investors have become the dominant force in Kazakhstan’s stock market in just a few years, a shift that is rapidly redefining how the country funds growth and allocates household savings.

Photo credit: Shutterstock

A new report by the Astana International Financial Centre (AIFC), released at the beginning of March, shows that individual investors now account for the majority of trading on the Kazakhstan Stock Exchange (KASE), marking a decisive break from a market once driven largely by institutions.

The report states that Kazakhstan has moved from a narrow, institution-led market toward a more inclusive system with mass digital access, but warns that the next phase will depend on whether this participation becomes “durable, long-term investing behavior.”

Rapid growth masks structural imbalance

The scale of expansion is significant. By September 2025, retail accounts reached 4.62 million at the Kazakhstan Central Depository, alongside 2.17 million accounts linked to the Astana International Exchange (AIX).

Retail investors accounted for 62.1% of equity turnover on the KASE in 2024 and 55.2% in the first nine months of 2025. Trading activity is accelerating just as quickly. Individuals executed 3.6 million transactions in 2024. That figure rose to 4.5 million in the first nine months of 2025 alone.

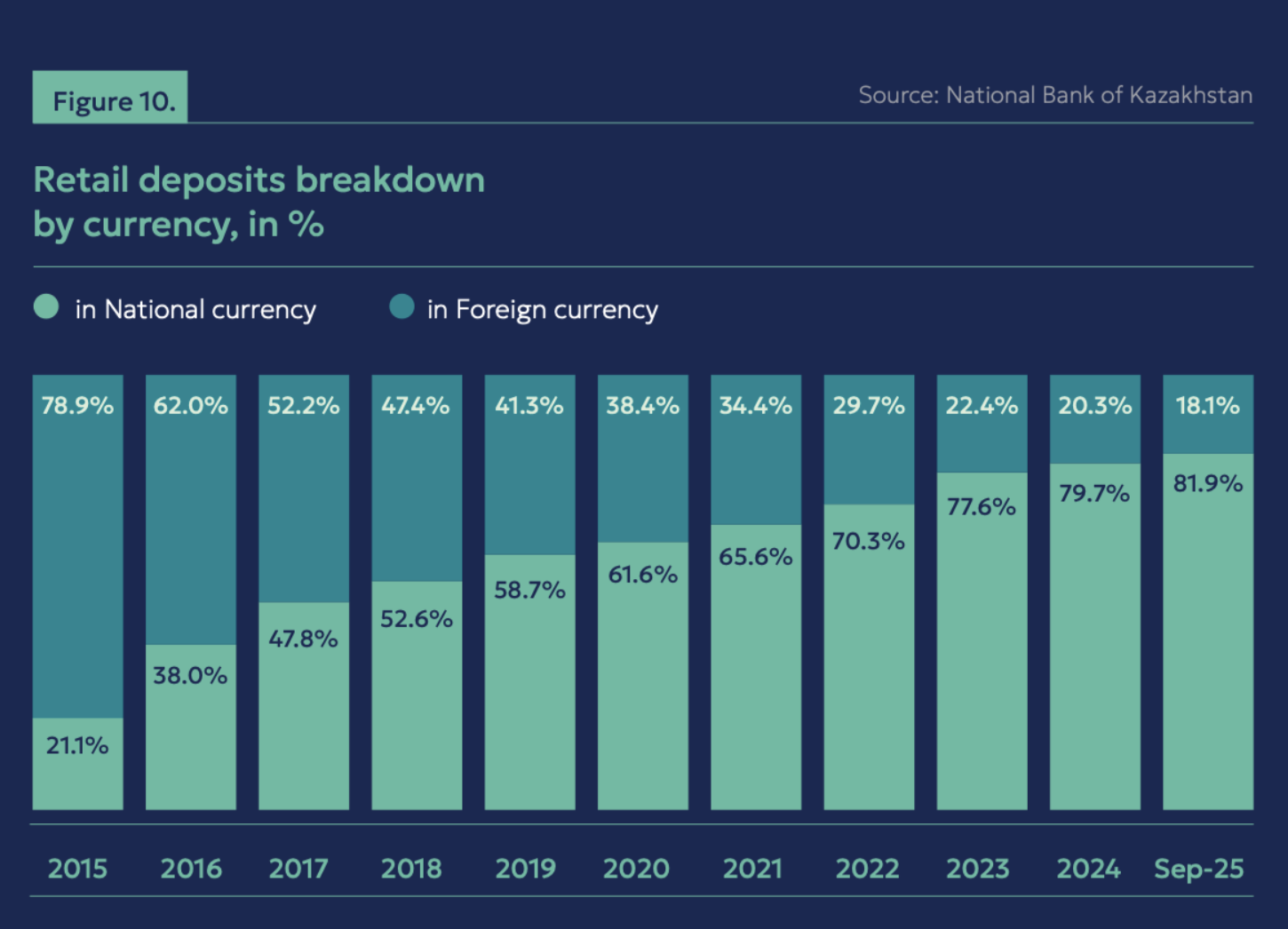

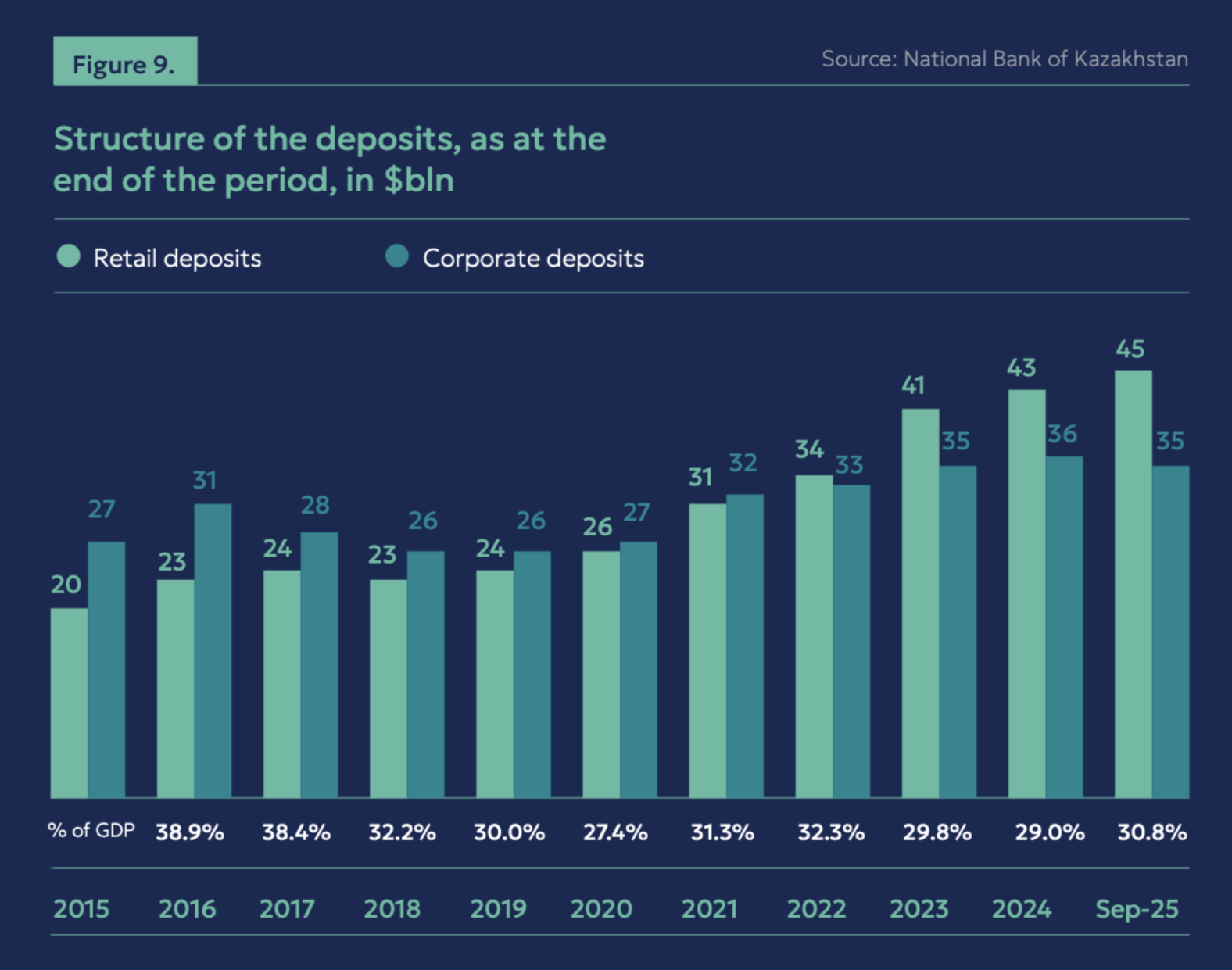

Yet the report draws a clear distinction between participation and capital allocation. According to the report’s data, deposits remain the main financial asset for most households, while real estate and foreign currency continue to dominate overall wealth. This gap suggests that Kazakhstan’s retail boom is broad but still relatively shallow.

Digitalization drives access and raises new risks

The report identifies digital infrastructure as the primary driver of this shift, with smartphones, remote identification and e-government infrastructure enabling banks and brokers to offer fully online onboarding and trading, reducing barriers to entry to near-zero levels. More than 90% of retail accounts have been opened in recent years.

That speed has changed the market’s composition almost overnight. However, it has also exposed a weakness. Financial literacy remains uneven, and participation often rises during IPOs or market rallies before fading again. In practical terms, access is scaling faster than understanding.

Kazakhstan’s market is expanding, but from a low base. The report cites markets such as the United States and the Nordic countries as benchmarks, where retail participation is more deeply embedded and can account for 30–40% of trading during periods of volatility. It also highlights Asia’s growing role, noting that around 60% of the world’s listed companies are now located in the region, accounting for roughly 31% of global market capitalization.

In Kazakhstan, these figures reach 21.8% of GDP. According to the report, the country’s stock market remains relatively shallow compared to developed economies, where capitalization typically reaches 150–170% of GDP.

According to the report, this imbalance matters because the market, dominated by retail flows but lacking depth, is more sensitive to sentiment and short-term movements. In more mature systems, retail investors tend to dominate trading primarily during periods of volatility. In Kazakhstan, that level of participation is becoming structural. The result is a market that is more inclusive, but also more reactive.

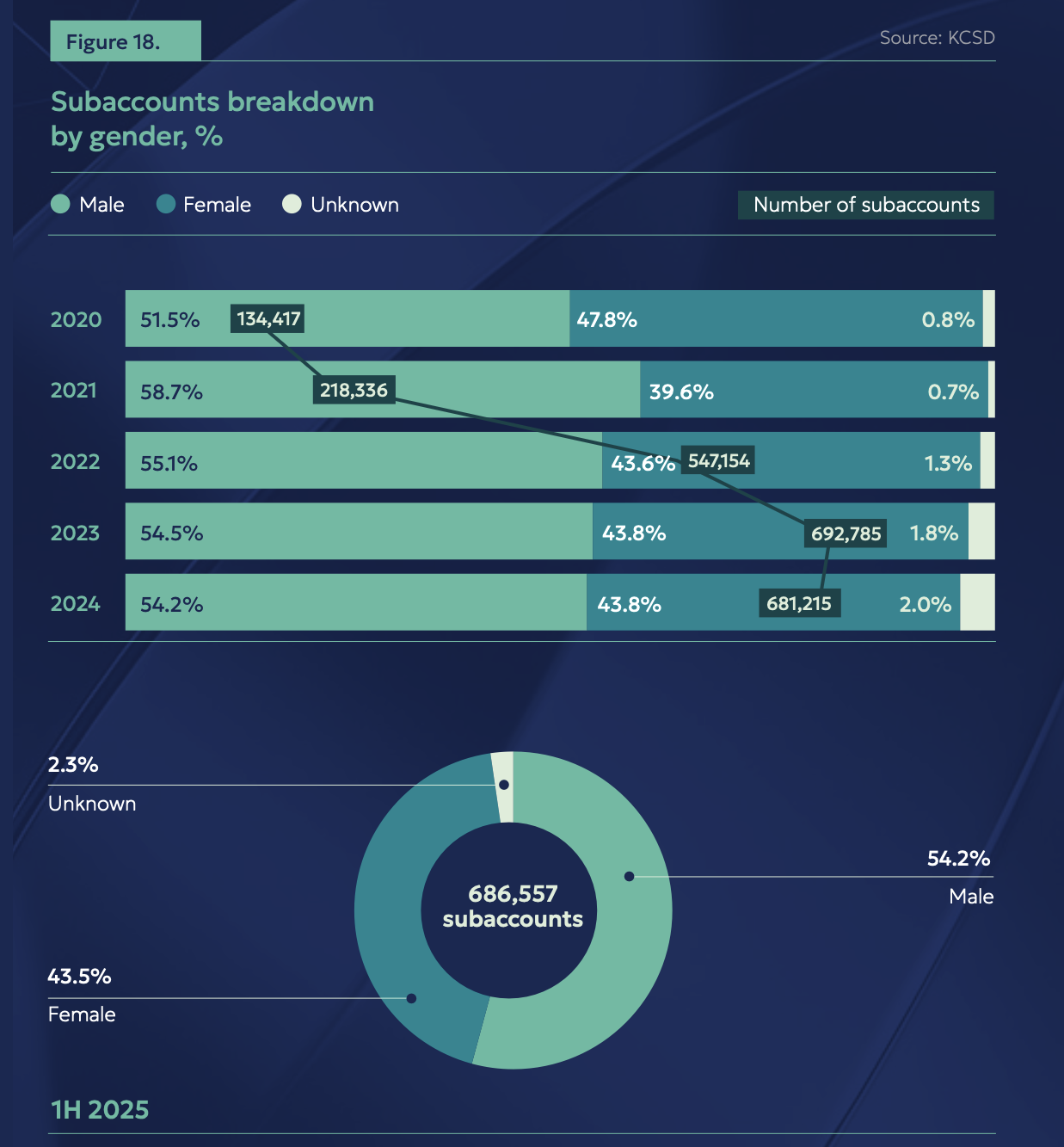

Women investors: smaller share with untapped potential

The report highlights a persistent gender gap in investment activity. Men account for roughly two-thirds of invested capital, while women represent about one-third. This imbalance points to a broader issue of participation. While access to markets has expanded, capital allocation remains uneven across demographic groups.

The report highlights a persistent gender gap in investment activity. Men account for roughly two-thirds of invested capital, while women represent about one-third. This imbalance points to a broader issue of participation. While access to markets has expanded, capital allocation remains uneven across demographic groups.

The report emphasizes the need to develop more stable, long-term investment behavior among retail participants. In this context, the report suggests that expanding participation among underrepresented groups could, over time, support a more balanced investor base.

Retail investors are increasingly moving beyond equities into higher-yield instruments, particularly corporate bonds. The share of individuals in this segment has grown significantly, rising from 3.8% in 2021 to 23.1% in 2025.

According to the report, the demand has been especially strong for bonds issued by microfinance organizations, reflecting their comparatively high coupon rates. The report notes that this shift has broadened access to investment products but has also raised concerns about investor protection and risk awareness. Higher returns are attracting new participants, even as the complexity and risk profile of these instruments increase.

The real constraint: behavior

The report’s central argument is that Kazakhstan’s challenge is no longer access, but behavior. The report notes that participation “frequently peaks around major offerings or strong market performance,” indicating that engagement remains inconsistent. Such a behavioral pattern limits the market’s ability to generate stable, long-term capital. It also increases volatility during downturns, when less experienced investors may exit as quickly as they entered.

According to the findings, retail investing is becoming a structural feature of Kazakhstan’s financial systems, influencing liquidity, pricing and even how the state approaches funding. However, the current trajectory is not guaranteed to produce a stable outcome.

Kazakhstan has succeeded in opening its markets. The harder task now is to ensure that participation becomes informed, sustained and resilient. Until that happens, the country’s retail investment boom will remain both a sign of progress and a source of underlying risk.