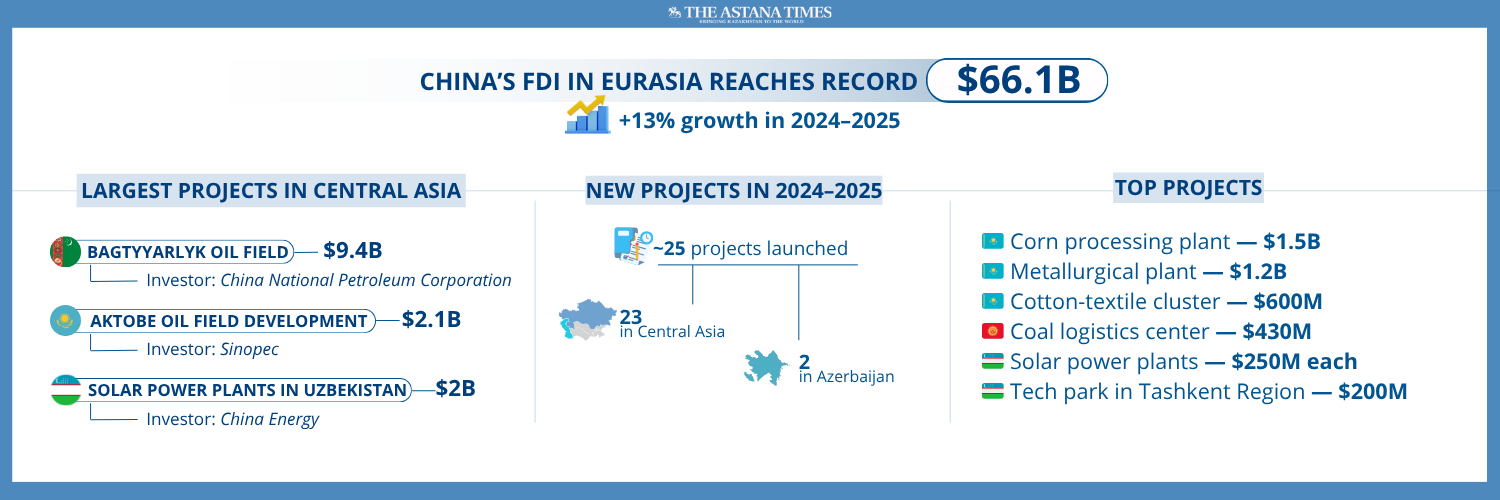

ASTANA – China’s accumulated foreign direct investment (FDI) in the Eurasian region has reached a record $66 billion, marking a 13% increase over 2024-2025, according to a report by the Eurasian Development Bank. Experts say investment patterns are shifting markedly, away from raw materials and toward manufacturing and energy.

Photo credit: Shutterstock

Alexander Zaboеv, head of the bank’s Center for Integration Studies, said total accumulated investment from Asian countries in the Eurasian region reached around $120 billion as of 2025, with China accounting for 55%.

“Chinese FDI in the region has grown steadily, rising from $37.3 billion in 2016 to $66.1 billion in 2025, an increase of nearly 80%, or around $30 billion in absolute terms. Chinese investments are present across all Eurasian countries, with the largest volumes concentrated in Kazakhstan, Mongolia, Russia, Afghanistan and Uzbekistan,” Zaboеv said.

Central Asia is China’s primary destination within the Eurasian region, with accumulated investment reaching nearly $36 billion. That share has grown by five percentage points over the past five years.

Central Asia at the core

According to Aidos Omarov, a senior analyst at the bank, Kazakhstan, Uzbekistan and Turkmenistan lead in country breakdowns, each receiving roughly $10 billion in accumulated Chinese investment.

“In terms of sectors, commodities historically dominated, but the past five years have seen sharp growth in manufacturing and electricity generation. Together with raw materials, these sectors now account for 85% of total Chinese investment in Central Asia,” Omarov said.

Omarov highlighted several major projects driving the numbers. In Turkmenistan, the development of the Bagtyyarlyk oil field with investment from CNPC has surpassed $9 billion, with further expansion planned.

In Kazakhstan’s Aktobe region, investments by CNPC and Sinopec in oil field development have exceeded $2 billion. In Uzbekistan, China Energy is financing the construction of three solar power plants across three regions, with a total investment currently around $2 billion.

Kazakhstan and Uzbekistan remain the largest recipients of Chinese investments, though trends differ sharply.

“Kazakhstan has historically been the top destination, but growth has been moderate, rising from $10.3 billion to $11.4 billion over five years. In contrast, Uzbekistan has seen rapid expansion, with investment jumping from $2.1 billion to $10.7 billion, more than a fivefold increase,” Omarov said.

He attributed Uzbekistan’s surge to a low starting base, economic liberalization, improved conditions for foreign investors, and growing demand for industrial and infrastructure modernization.

The two countries also diverge sectorally. In Kazakhstan, commodities have historically dominated, but manufacturing’s share has grown from 13% to 18% over the past five years, while the commodities share has declined to 46%.

In Uzbekistan, manufacturing was traditionally the largest sector, but since 2022, electricity, driven largely by renewable energy projects including solar and wind, has surged to account for more than half of China’s entire investment portfolio in the country.

Mongolia: stable but specialized

According to Omarov, Mongolia remains an important but highly specialized market, focused almost entirely on extractive industries. Chinese investment there increased from $8.2 billion in 2016 to $10.3 billion in 2025. However, it has stabilized in recent years, indicating a shift from active investment to project operation.

“Around 68% of investment in Mongolia is concentrated in metal ore mining, with the remaining 32% in oil and gas. Major deals include roughly $2 billion investments in iron ore assets and a similar-sized acquisition in the oil sector,” he said.

New wave of projects signals shift

The report also highlighted new projects launched between the second half of 2024 and the first half of 2025. Around 25 projects were initiated during this period, with 23 in Central Asia and two in Azerbaijan. By the number of projects, Uzbekistan leads, while Kazakhstan dominates in total investment value, driven by several large-scale initiatives.

“These include a $1.5 billion corn processing plant in the Zhambyl Region by Fufeng Group, a $1.2 billion metallurgical plant expected to produce up to 3 million tons of steel annually, and a $600 million cotton-textile cluster in the Turkistan Region. In Uzbekistan, key projects include two 250-megawatt solar power plants, each valued at about $250 million, an Uzbek-Chinese industrial zone in Almalyk with planned investments of $200 million, and a $140 million waste-to-energy plant in Andijan,” Omarov said.

A major project in the Kyrgyz Republic involves the construction of a coal logistics center on the Kyrgyz-Chinese border, with investments estimated at $430 million.

Omarov identified four key trends shaping Chinese investment in Eurasia: a shift from extractive industries to manufacturing and energy, rapid growth in Uzbekistan’s share, increasing participation of private capital, and expansion of greenfield projects.

The share of manufacturing and energy projects has doubled over the past decade, from 17% to 34%, while Uzbekistan’s share of Chinese investment rose from 1% to 16%.

“Private sector participation has also grown, with its share increasing from 22% to 27% over the past decade, a sign of improving investment conditions. Meanwhile, greenfield projects expanded from 43% to 60% of China’s investment portfolio in the region, reflecting long-term commitments and contributing to industrial development and job creation,” Omarov said.