ASTANA — Kazakhstan’s mining sector sits on a paradox. It holds some of the world’s most strategically relevant mineral reserves, yet struggles to attract capital where it matters most at the earliest and riskiest stages of exploration. As global demand for critical minerals accelerates, the constraint is no longer geology, but the ability to turn potential into assets investors can trust.

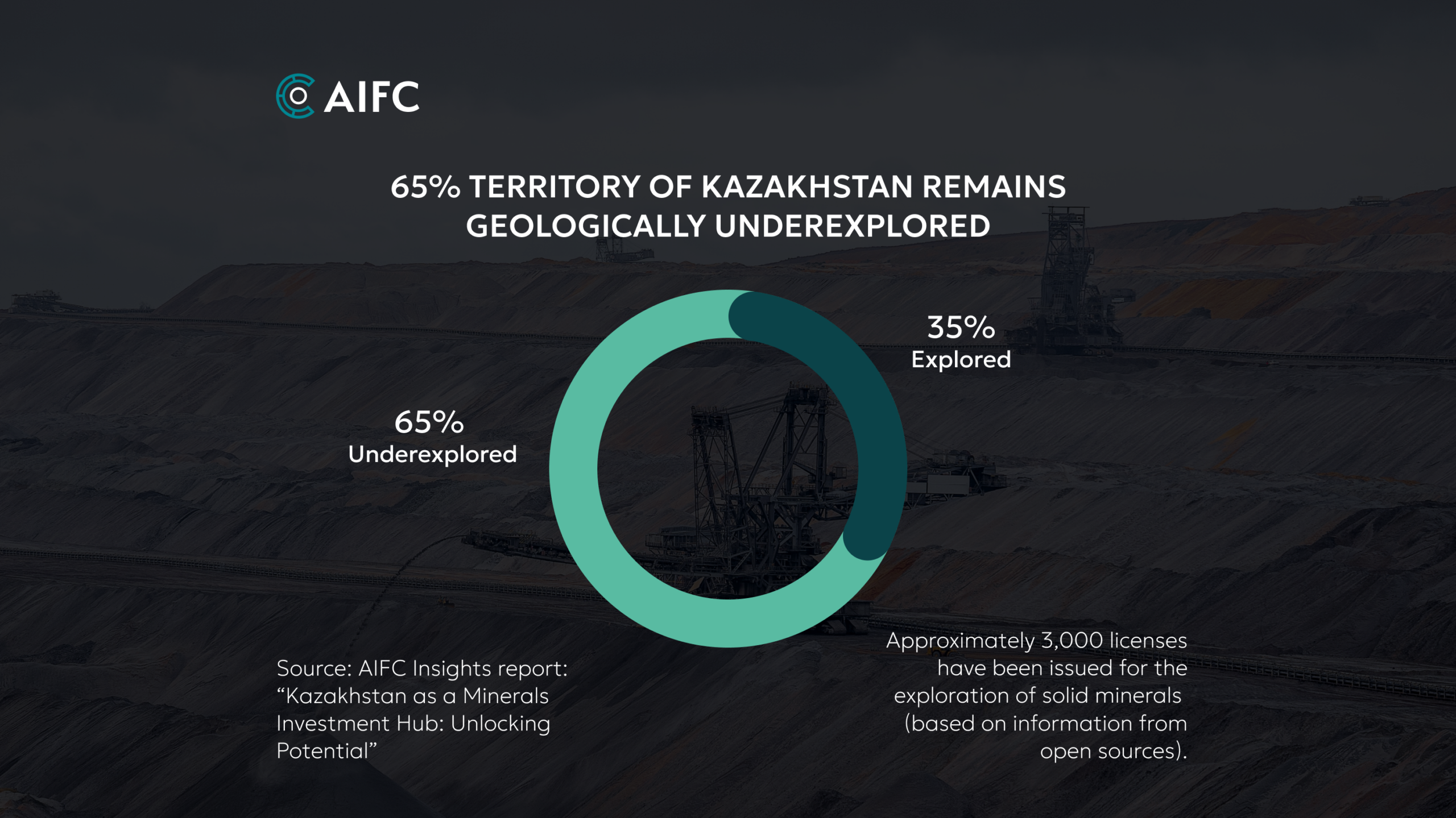

Today, around 65% of Kazakhstan’s territory remains geologically underexplored. While approximately 3,000 exploration licenses have been issued, their development ultimately depends on attracting investment. A key constraint lies in how mineral reserves are reported and verified.

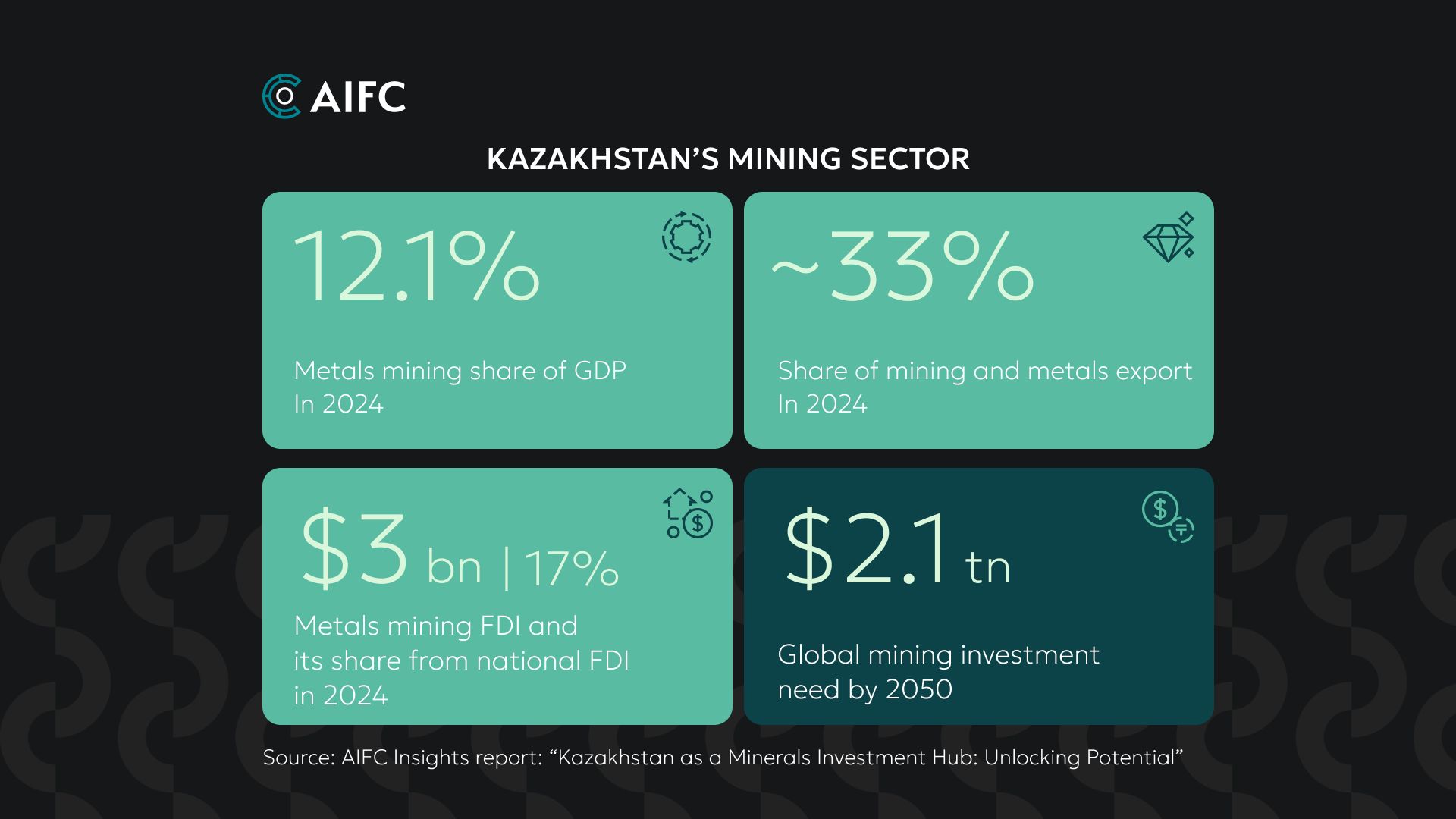

According to the AIFC report titled Kazakhstan as a Minerals Investment Hub: Unlocking Potential through the AIFC, the mining sector accounted for 12.1% of GDP, 16.1 trillion tenge (US$34.1 billion) in 2024, and approximately 33% of total exports, underscoring its structural role in the economy.

Metallurgy and mining projects represented 17% of total foreign direct investment, or around $3 billion, with FDI in the sector doubling compared to 2019 despite an overall decline in national inflows.

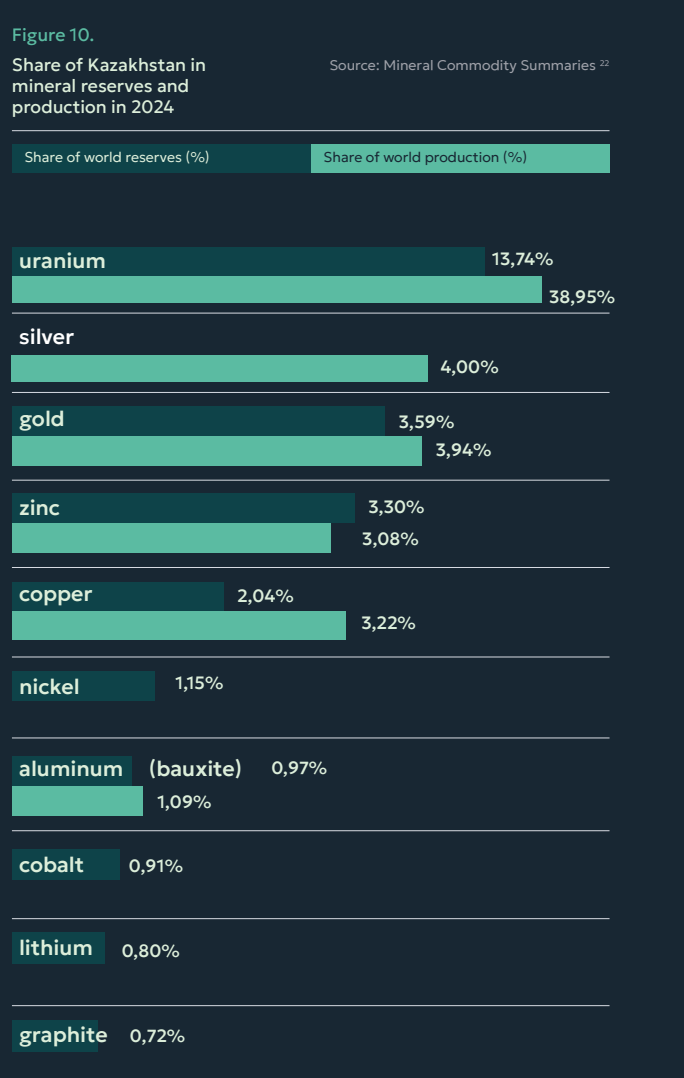

The country holds significant reserves of copper, gold, chromium, and rare earth elements, while remaining the world’s largest uranium producer.

International investors typically rely on standardized frameworks such as the JORC Code, a globally recognized system that sets clear rules for assessing and disclosing exploration results and reserves. These standards are designed to make projects comparable, transparent, and, crucially, bankable.

In Kazakhstan, however, a significant share of reserves is still classified under legacy systems or has not yet been fully aligned with international reporting standards such as JORC or the national KAZRC framework.

This creates a structural bottleneck. Exploration risk is high, data is often incomplete or not standardized, and investors face difficulty assessing project viability. In practice, this reduces the pool of capital willing to engage at the earliest stages.

A global problem with local implications

Barry describes, the sector remains fragmented, with “everyone operating kind of solo.” Photo credit AIFC

Kazakhstan’s situation reflects a broader shift in the global mining sector. After a decade of underinvestment in exploration, the industry is now facing a shortage of discoveries just as demand for critical minerals accelerates. As Tim Barry, Arras Minerals Corporation CEO, noted the sector is “suddenly finding that we haven’t spent enough time trying to find them.”

“I think the key factor is new discoveries. We’ve entered a period where we have had for the last decade an underinvestment in exploration and now the world needs a lot of critical minerals. We’re suddenly finding that we haven’s spent enough time trying to find them. So if I was to put the number one issue, it’s investment into exploration to find new resources,” said Barry.

At the same time, “the new resources” are becoming more selective. Exploration budgets remain concentrated, with around 70% of global spending directed to a limited number of jurisdictions. In this environment, projects that lack standardized reporting, clear timelines, or visible development pathways struggle to compete.

The structure of the exploration market further complicates capital allocation. Early-stage projects often operate in isolation, limiting visibility and making risk assessment more difficult. As Barry describes it, the sector remains fragmented, with “everyone operating kind of solo.”

The financial ecosystem gap

The core issue is not simply the availability of capital, but the conditions under which it can be deployed. Junior mining companies, which dominate early-stage exploration, face persistent constraints driven by high risk perceptions and underdeveloped financial mechanisms.

These projects are typically long-term, capital-intensive, and generate no revenue during the exploration phase. According to Said Sultanov, founder of Aurora Minerals Group, the process from discovery to production can take between 10 and 15 years.

Sultanov explains that the process from discovery to production can take between 10 and 15 years. Photo credit AIFC

“The process of geological exploration is very long. From the search to the launch of the site, that is, to the discovery, it can take up to 10-15 years. Accordingly, the financing of such projects is time consuming,” said Sultanov.

During this period, companies rely entirely on external financing, according to Sultanov, even though junior firms account for 60–70% of global mineral discoveries.

“It’s no secret that the issue of financing geological exploration is a very painful issue for many juniors, because, as a rule, they do not get anything, they have no income. And in all this, they need this process the most,” said Sultanov.

The mismatch is clear: the segment responsible for most discoveries is also the least able to secure funding. Limited reserve verification compounds the issue.

Without alignment to international reporting standards, projects remain difficult to evaluate and price. Combined with the absence of a structured pipeline of screened projects, this reduces investor confidence and slows capital deployment. In effect, investors are not choosing between projects. They are choosing whether to engage with uncertainty they cannot fully quantify.

An attempt to structure the market

Recent initiatives suggest an effort to address these constraints. The Astana International Financial Centre (AIFC) has launched a Junior Mining Platform on April 14 to improve access to capital for early-stage exploration. The platform is designed to create a more structured pipeline of projects, introducing screening mechanisms and facilitating connections between investors and junior mining companies. It also plans to incorporate financing instruments commonly used in international markets, including royalties, streaming, and earn-in agreements.

AIFC Authority Chief Product Officer Zhanbolat Kakishev noted that the sector’s main challenge is the “lack of structured access to capital at the early stages.”

“The platform is designed to address precisely this issue. We are creating a transparent and accessible environment where projects can secure financing at an early stage, while investors can gain access to a database of projects selected according to industry-recognized criteria,” said Kakishev.

The logic is straightforward: reduce fragmentation, improve transparency, and make early-stage projects easier to assess. Yet the effectiveness of such mechanisms will depend on whether they can alter investor perception of risk. Structuring deal flow does not eliminate geological uncertainty. It only makes it more visible.

The global outlook

Globally, the opportunity is expanding. Capital demand in the extractive industries is projected to reach $2.1 trillion by 2050, driven by the energy transition and the growing material intensity of modern economies.

Kazakhstan’s geographic position, between China, Europe, Russia, and South Asia, reinforces its role as a potential supply chain node, particularly within emerging transport corridors. At the policy level, measures such as granting priority rights to exploration investors and expanding geological survey coverage from 1.5 to 2.2 million square kilometers aim to reduce entry risks and signal state support.

Kazakhstan’s geographic position, between China, Europe, Russia, and South Asia, reinforces its role as a potential supply chain node, particularly within emerging transport corridors. At the policy level, measures such as granting priority rights to exploration investors and expanding geological survey coverage from 1.5 to 2.2 million square kilometers aim to reduce entry risks and signal state support.

Within Central Asia, this combination of resource endowment, regulatory adjustments, and investment incentives positions Kazakhstan as a relatively attractive destination for capital. However, the structure of its resource base complicates this picture.

The sector is dominated by greenfield opportunities, with few advanced brownfield projects ready for near-term production. In addition, over 20 billion tons of mineral waste and secondary formations represent a potential but capital-intensive source of critical materials. At the same time, most reserves are still classified under the Soviet-era GKZ system, a legacy reserve classification framework used in the Soviet Union. This limits comparability with international frameworks such as the Committee for Mineral Reserves International Reporting Standards (CRIRSCO).

Kazakhstan ranks 11th globally in copper reserves, 7th in zinc, 11th in bauxite, and 8th in lead, while also holding underdeveloped deposits of lithium, nickel, and rare earth elements. All these minerals are central to the energy transition.

These factors support its ambition to become a key supplier in global critical mineral supply chains. However, resource potential alone is no longer sufficient. Global capital is increasingly directed toward jurisdictions that offer not just resources, but clarity in regulation, reporting, ESG standards, and project development pathways. In this context, Kazakhstan’s challenge is less about attracting attention and more about meeting the conditions required for sustained investment.